Beta is live — Know if your edge is real

Test your strategy

before you invest

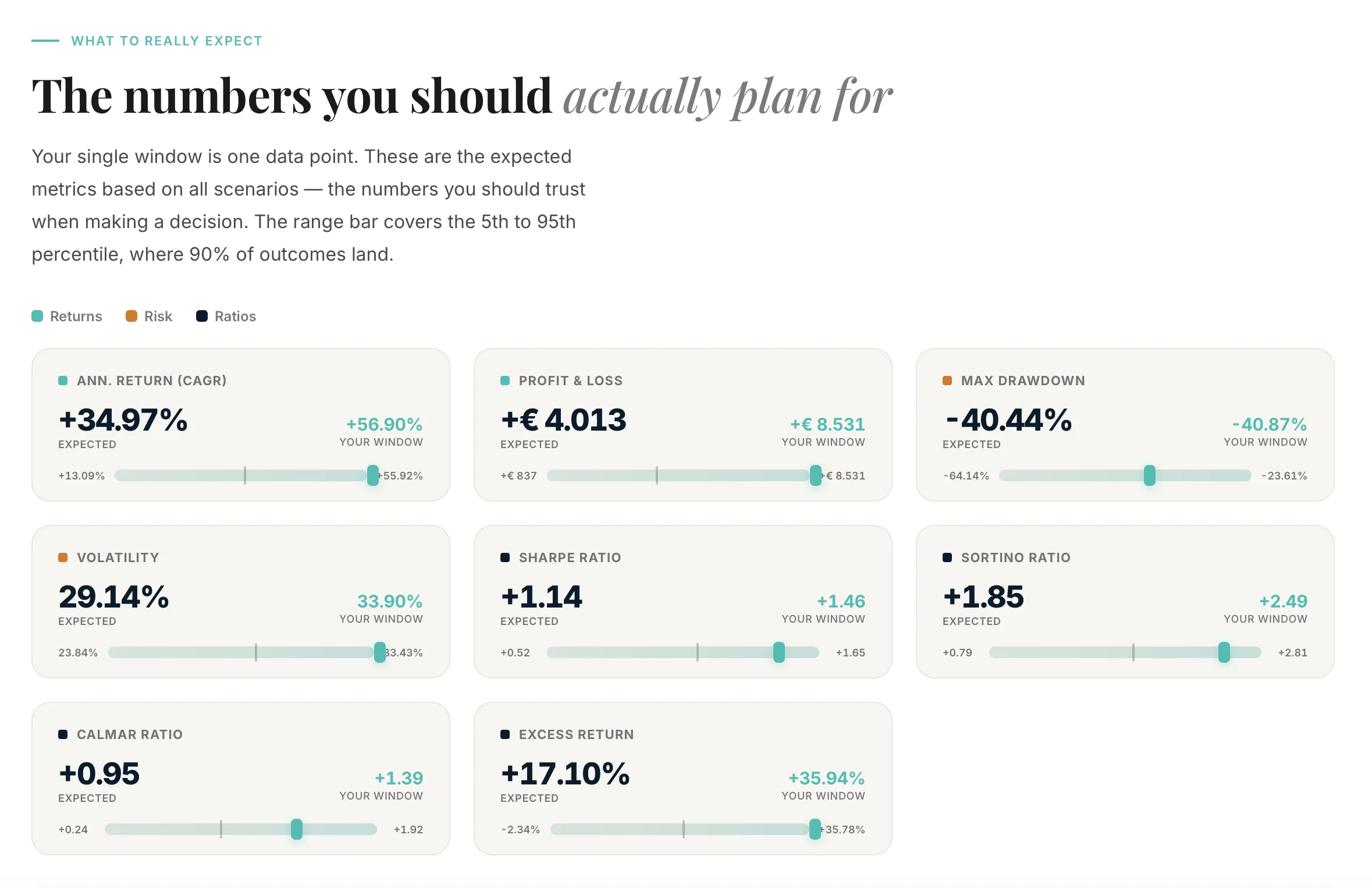

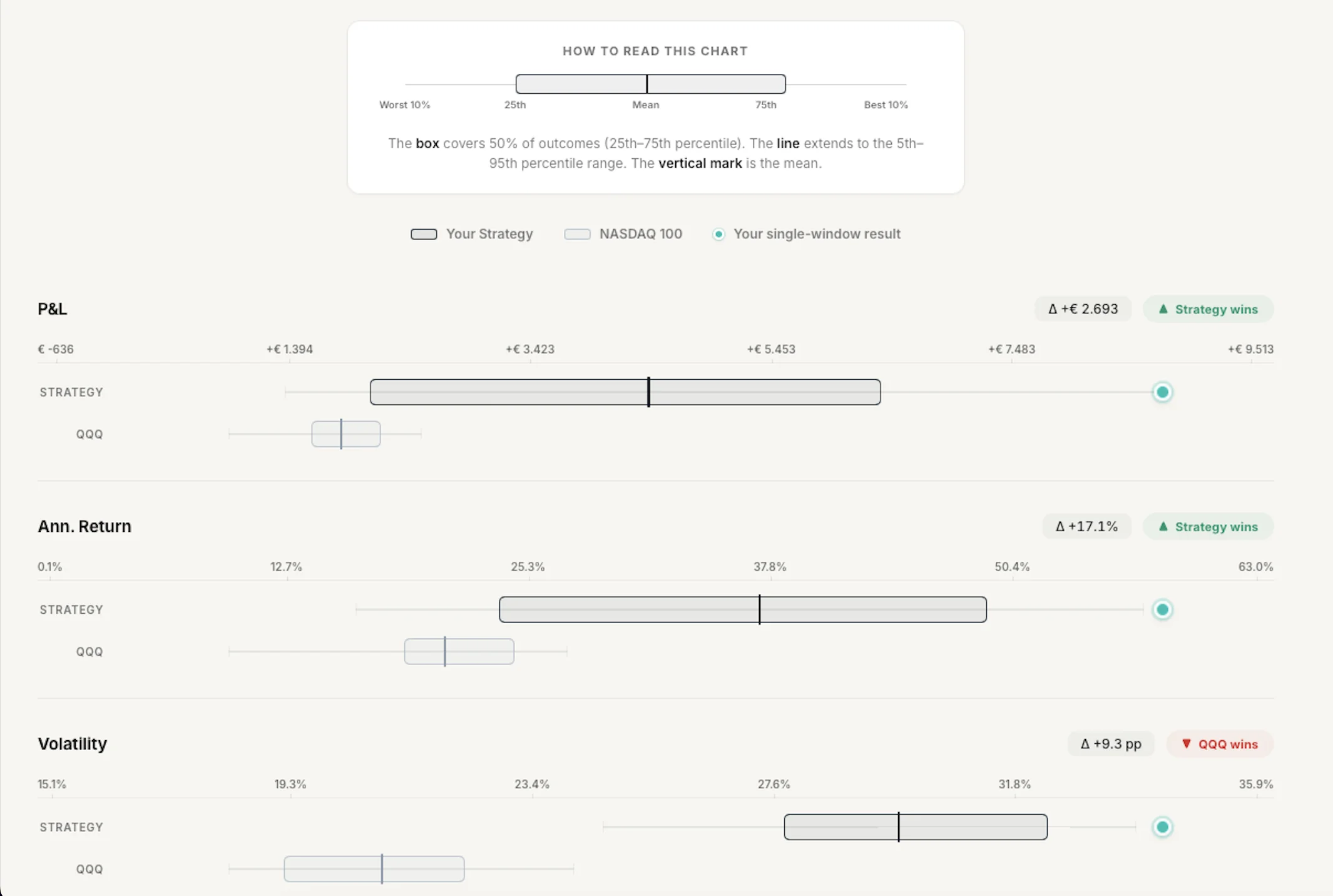

Backtest any investment strategy against historical data. Stress-tested across 50 rolling market windows — so you know if your edge is real, or just luck.

No credit card required · Free tier available